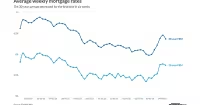

The average rate mortgage loan on a 30-year fixed mortgage fell to 5.98% in February, its lowest point since September 2022, giving homebuyers and homeowners a little more room to work with just as the spring market gets going. Freddie Mac said that as of April 23, the average rate had edged back up to 6.23%, but it still stood at its lowest level in the last three spring homebuying seasons.

For people thinking about relocating or downsizing for retirement, the drop can matter in a very practical way. Lower interest rates can make a move easier to afford, and in some cases they can make it possible to sell a larger home and buy a smaller one without taking on a fresh mortgage at all. One example: a homeowner who sells a $700,000 house and nets $500,000 after paying off the remaining mortgage may be able to buy a new $500,000 home outright.

The rate picture also keeps refinancing in play for borrowers with older loans. The article said a refinance is often worth considering when the new rate is at least one percentage point below the old one, and gave the example of a borrower paying 7.5% who could find a promising opportunity at 6.25%. That kind of spread can be enough to justify the paperwork and closing costs for some households, especially if they expect to stay in the home for years.

There is still a catch. Rates are lower than they were at many points over the past two years, but they are not back to the deeply cheap levels that helped fuel the housing market earlier in the decade. Shorter-term loans can trim total interest costs, but they usually come with somewhat higher rates, so the tradeoff is cost now versus savings over time. For retirees, near-retirees and anyone trying to reset their housing costs this season, the window is open — just not wide.